Reliance on Third-Parties

In some situations where you are dealing with a client who is an intermediary or reseller and is independently regulated for AML Activities, it may be possible to rely on the intermediary to apply appropriate customer due diligence measures.

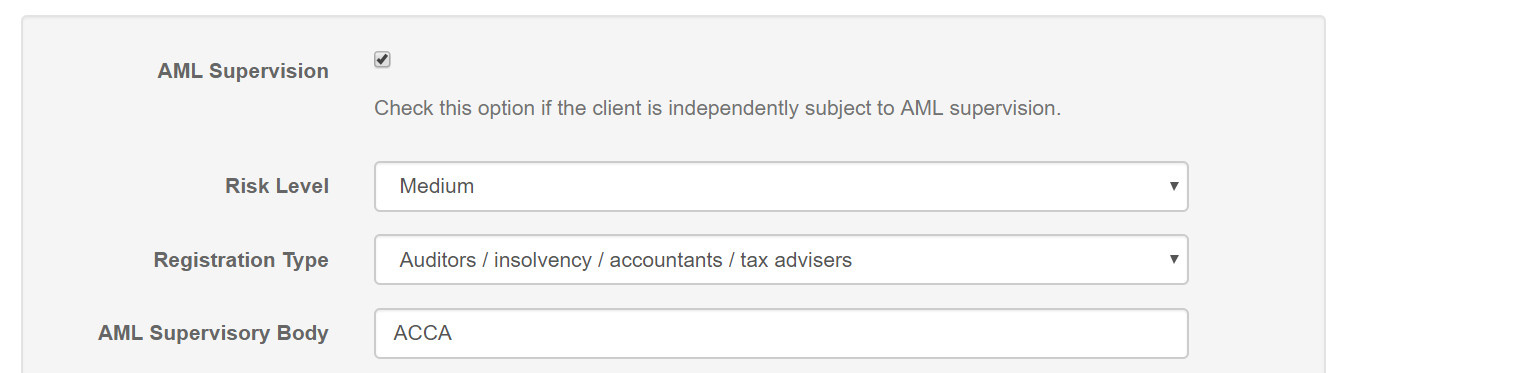

When entering a client record there is an option under the “Risk Profile” tab to indicate that the client is independently regulated and under AML Supervision.

You can also provide some additional information here to record the client’s business activity and supervisory body.

According to HMRC guidelines (as of December 2017), the persons that may be relied upon are as follows:

In the UK

- A credit or financial institution which is authorised by the FSA.

- An auditor, insolvency practitioner, external accountant, tax advisor or independent legal professional who is supervised for the purposes of the Money Laundering Regulations 2007 by one of the following professional bodies

– Association of Chartered Certified Accountants

– Council for Licensed Conveyancers

– Faculty of Advocates – General Council of the Bar

– General Council of the Bar of Northern Ireland

– Institute of Chartered Accountants in England and Wales

– Institute of Chartered Accountants in Ireland

– Institute of Chartered Accountants of Scotland

– Law Society

– Law Society of Scotland

– Law Society of Northern Ireland.

In EEA states

- A credit or financial institution, auditor, insolvency practitioner, external accountant, tax advisor or independent legal professional who is:

– subject to mandatory professional registration recognised by law, and

– supervised for compliance with the requirements of the money laundering directive.

In a non-EEA state

- A credit or financial institution (or equivalent institution), auditor, insolvency practitioner, external accountant, tax advisor or independent legal professional who is:

– subject to mandatory professional registration recognised by law

– subject to requirements equivalent to those laid down in the money laundering directive, and

– supervised for compliance in a manner equivalent to the standards set out in section 2 of chapter V of the Money Laundering Directive.In regulation 17, ‘financial institution’ excludes money service businesses.

Policy and decisions on whether to rely on third-parties should be part of the risk-assessment and include the obtaining and consideration of relevant information on the status and background of the third-party. The business must put appropriate procedures in place to ensure that the customer due diligence checks are carried out correctly and must take steps to ensure that the third-party will, if requested, provide any information on the customer (and any beneficial owner) which the third-party obtained when they applied the customer due diligence measures. Section 11 of this guidance provides further information on these record keeping requirements. Businesses must not rely on any third-party who is bound by confidentiality requirements not to provide details of the identity of the customer or any beneficial owner, as the business needs to know who their customer is in order to comply fully with the Money Laundering Regulations 2007. Businesses can find further information on reliance on third-parties in the JMLSG guidance.